When an apartment syndicator analyzes the results of their underwriting, and when a passive investor is deciding whether to invest in a syndicator’s deal, the two main return factors they focus on are the cash-on-cash return and the internal rate of return.

In this blog post, you will learn the definitions of these two important return factors, how they are calculated, and why they are relevant in apartment syndications.

What is Cash-on-Cash Return?

Cash-on-cash return (commonly referred to a CoC return) is a factor that refers to the return on invested capital. CoC return is the relationship between a property’s cash flow and the initial equity investment, which is calculated by dividing the initial equity investment by the cash flow. For the purposes of the CoC return calculation for apartment syndications, cash flow is the profits remaining after paying the operating expenses and debt service.

There are actually two different versions of the CoC return for apartment syndications: including profits from sale and excluding profits from sale. The CoC return factor excluding profits from sale will show passive investors how much money they should to expect to receive for each distribution during the hold period, as well as an average annual return on their investment property.

The cash on cash vs irr or cash on cash return vs irr multiple factor including the profits from sale will show passive investors how much money they should expect to make from the project as a whole.

In order to calculate both CoC return factors, you need the initial equity investment amount, the projected annual cash flows, and the projected profit from sale for both the overall project and to the passive investors.

Here is an example of how to calculate CoC return for an apartment project:

Passive investors aren’t as concerned about the overall project’s CoC return but more so the CoC return to the limited partners (LP).

LIKE THIS ARTICLE SO FAR? THEN YOU’LL REALLY WANT TO SIGN UP FOR OUR NEWSLETTER. IT’S SENT ONCE A WEEK AND PACKED WITH OUR BEST INVESTING TOOLS, ARTICLES AND STUFF YOU WON’T FIND ANYWHERE ELSE ONLINE. SUBSCRIBE OVER HERE.

Here is an example of how to calculate the CoC returns to the limited partners based on an 8% preferred return and 70/30 profit split:

In this example, the average annual CoC return to the LP is 8.33%, which is good because it is above the preferred return offered. The overall CoC return for the five years is 185.72%. So, someone who invested $100,000 would make $85,720 in profit.

However, as you can see in the example above, the CoC return to the limited partner is below the preferred return percentage in years one and three. So, for this deal, the syndicators options are to review their underwriting assumptions to see if they can increase the cash flow, have the preferred return accrue and pay the accrued amount at sale or when the cash flow supports it (i.e. end of year two to cover the year one shortfall), or pass on the deal.

A “good” CoC return metric is subjective and based on the goals of the syndicator and the passive investors. However, a good rule of thumb is a minimum average CoC return excluding the profits from sale equal to the preferred return offered to the limited partners.

What is Internal Rate of Return?

The main drawback of the cash-on-cash return metric is that it doesn’t account for the time value of money. For example, receiving a 185.72% CoC return over a 5-year period is very different than receiving the same CoC return over a 10-year period or a 1-year period. That is where internal rate of return comes in.

The technical definition of internal rate of return (commonly referred to as IRR) is the interest rate that makes the net present value of all cash flow equal to zero. In layman’s terms, this equates to a project’s actual or forecasted annual rate of growth by isolating the effect of compounding interest if the investment horizon is longer than one-year, which CoC return does not.

If you have the data to calculate the CoC return, you can calculate an CoC vs IRR for the overall project and to the passive investors. What is needed is the initial equity investment and the annual cash flows, with the final year including the profit from sale.

The IRR formula is complex (click Internal Rate of Return if you want to see the full formula), so for simplicity, the IRR() function in excel should be used.

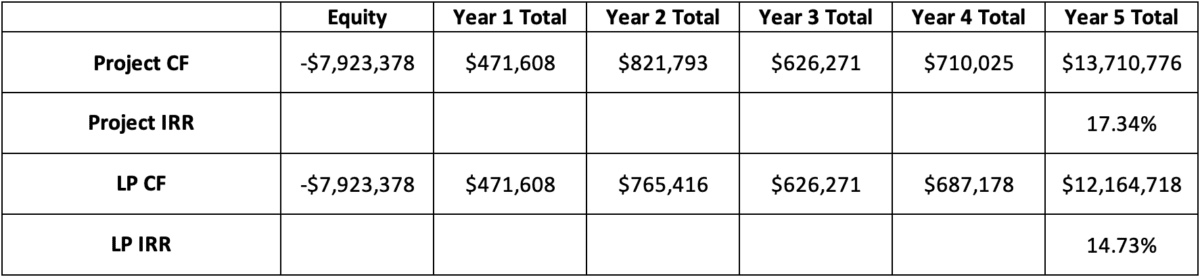

Following the same example, here is the 5-year IRR for the overall project and for the limited partners:

Another IRR metric is XIRR. For the regular IRR calculation, the assumption is that the cash flows are distributed on a fixed, periodic schedule (i.e. annually, monthly, quarterly, daily, etc.). The XIRR function calculates the internal rate of return when cash flows are distributed on an irregular period.

In order to calculate XIRR, the additional data required are the exact days that the cash flow was distributed. Examples of instances where the XIRR would come into play are when the syndicator refinances or secures a supplemental loan to return a portion of the passive investors’ equity and when the syndicator sells the asset since the closing date likely will not be exactly 1, 2, 3, etc. years after purchasing the deal.

A “good” IRR metric is also subjective and based on the goals of the syndicator and their passive investors. For my company’s deals, we want a 5-year IRR to the limited partners of at least 15%.

The main difference cash on cash between irr and cash on cash or cash on cash return vs irr and internal rate of return metric is time. If the investment is held for one-year, difference between irr and cash on cash then the two return metrics are interchangeable. But if the projected hold period is more than a year, internal rate of return is more accurate.

Are you a newbie or a seasoned investor who wants to take their real estate investing to the next level? The 10-Week Apartment Syndication Mastery Program is for you. Joe Fairless and Trevor McGregor are ready to pull back the curtain to show you how to get into the game of apartment syndication. Click APARTMENT SYNDICATION MASTERY to learn how to get started today.

Disclaimer: The views and opinions expressed in this blog post are provided for informational purposes only, and should not be construed as an offer to buy or sell any securities or to make or consider any investment or course of action.