For realtors and investors, planning ahead is one of those things that separates winners from losers. Online searches for what causes housing market value to crash keeps growing. Millions are wondering if there will be a housing market crash in 2023, seeking advice on what to do when the housing market crashes.

While odds are that we won’t witness a housing market crash in 2022, when is the next house market crash? Will home prices drop in 2023?

This article is a sort of fear-setting or worst-case-scenario approach to real estate market predictions. What 2020 clearly showed us is that it’s usually hard to predict the ebbs and flows of real estate.

If you want even more real estate market updates (like this) and our very best investing tips, you can get them in our Sunday newsletter (loved by 14k+ investors).

No one could have thought there would be an influx of millennial first-time home buyers pouncing on home valuations while the coronavirus vaccine was still in view. Real estate activity in 2020 had a significant effect on the United States economy’s rebound.

So, I asked some real estate experts the question:

If the housing market crashes in 2022, how would you keep your business afloat? Here are the responses I received.

Jeb Smith, Broker Associate and GRI with Coldwell Banker Realty in Huntington Beach

“I want to be clear that I don’t believe there will be a ‘housing market crash’ in 2022, but if the home market were to change, I would do exactly what I’ve done my entire career, and that’s focus on relationships. As a realtor who receives the majority of his business from past clients, friends, and single family, I would continue to nurture those relationships and be a source of information to help guide them through the tough times ahead.

“At the same time, I have experience in selling foreclosures in the last housing crisis debacle and would work on redeveloping those relationships to take advantage of any new opportunities that could arise. I don’t believe you need to change your business model entirely if you’ve been focused on the right things the whole time, so I would just continue to focus on those people that know me, like me, and trust me, and things will be just fine.”

According to Ken, there are four main opportunities for investors right now in the housing industry market:

1. Cost to Build vs. Cost to Buy

“Let me give you an example: Right now we are in the process of buying a property in Katy, Texas. We’re buying two apartment complexes of 648 units in Katy and paying $73 million for both projects. That’s under $130,000 per unit, which equates to $120–$130 per foot.

So, I’m buying a property at well below the cost to build. If I was to build another property values right next door to that property, it would be well over $200 per foot. In Phoenix, that same exact property prices we bought in Katy, Texas will cost a little over $200,000 a unit.

And of course, we went record low to Katy because the rents are not that much different because the property is right across the street from the Texas Medical Center.”

In other words, give more weight to locations where buying estate is comparatively cheaper than building costs — employ considerable due diligence.

2. Housing Supply vs. Housing Demand

“Take a look at the home supply and demand — where are people going? What’s the occupancy? If occupancy is really high in an area or about ready to be record high because the area is growing, then that means that your rental housing supply and demand is going to be there, and rents will grow like we just saw for the last 10 years in Austin, Texas.”

3. Follow the People

“People vote with their pocketbooks and their feet — the rider trucks, the U-Hauls, etc. Florida, Texas, and Arizona are good real estate markets right now. But it’s very hard to buy properties in many places because people are moving there right now. And you’re going to see rental interest rates go up in these places because people are buying properties for investment properties and renting them for the long term.”

4. Cash Flow vs. Capital Gain

“Don’t buy properties for capital gains. This is not the time, for example, to buy a home for $300K and flip it for $400K. You want to make it cash flow. You want to use the strong rental interest rates so that whatever you buy will put cash in your pocket over the long term and you’re building a primarily tax-free passive income.”

Expert Advice From Commercial Real Estate Pros

Kristina Morales, Realtor, KristinaMorales.com

“Regardless of the condition of the housing market, I am confident that my business will stay afloat. The market is currently going hot. However, it is hot for sellers, not buyers. So, when it shifts to a buyer’s market, it will be a hot market for buyer demand.

“For me, there are a few key things that I plan on doing to position my business for sustainable success. The first key to my business is to continue to invest in the right places — systems, automation, marketing, and people.

“Another key is anticipating market shifts and being nimble enough to skill up and prepare for the new market conditions. For example, if we find ourselves in market conditions where short house sales become prevalent, then I will be sure to prepare myself for this environment.

“The last key is to continually innovate. The client experience is the number-one driving force in my success, and constantly trying to innovate to improve and deliver home value to my clients is essential.”

Bill Gassett, Realtor and Owner of Maximum Real Estate Exposure

“When markets correct themselves, it is important for agents to be ready to adjust. It is very difficult to go from having to do little work to sell a house to all of a sudden having very few people to work with.

In the last significant real estate downturn from 2007 to 2012, there were significant hardships. Numerous existing homeowners lost substantial equity in their new homes. The chief economist was awful, and people were losing their jobs.

“This led to many financial crisis hardships including foreclosure. As an agent, I began to notice fairly quickly there was a housing demand for someone who could help homeowners short sell their property rather than letting it go to foreclosure. To keep my business running full steam ahead, I became a short-sale expert.

“While other agents were floundering, my business skyrocketed. Doing short sales in addition to my traditional business, I was doing 80–100 transaction sides by myself. Needless to say, these were some of the best-earning years of my career.

“All great recession real estate agents need to be able to adjust to their environment. Whether that means learning something new, investing more money back into their business, or doing something different. Change is inevitable.

A real estate correction will happen again. It always does. Agents who can recognize this early on will be able to put themselves in a better position not to skip a beat.”

Marina Vaamonde, Real Estate Investor,HouseCashin.com

“Experienced housing investors realize that the economy works in cycles and that they have to prepare for housing market slowdown times. In tough times, cash is definitely king. Investors who recently got into the market have probably not had time to set aside reserves. Even some experienced investors ignore the need for adequate reserves. They had better start now.

“High home prices make this a good time to sell properties that you previously bought at lower home prices and have held onto. Investors with a sizable portfolio should consider selling some assets to increase their bankroll.

Short-term investors with properties that are market-ready are in a good position. If the rapid acceleration of housing price increases results in a housing crash, there will be opportunities for those who have cash to spend.

“Decreased demand will probably not last long. There was already a housing supply shortage prior to the pandemic. According to Freddie Mac, the United States had a housing shortage in 2018 of 2.5 million units. With the right preparation now, a housing investor will still be in business if the housing market price declines”

Aleksandr Pritsker, Realtor and Founder of Team Blackstar at eXp Realty Crash

So, I try to make sure that I’m fully prepared for any market scenario and have the right contacts to be able to thrive and succeed in any market data that may come up. You never know what tomorrow will bring, but you always have to surround yourself with the right business people to keep you going no matter what the situation is.”

Jordon Scrinko, Realtor, precondo.ca

“The great recession thing about real estate, in general, is that transactions occur regardless of house price appreciation. Many people have to buy and sell homes for a number of reasons — jobs, relocation, upsizing, downsizing, etc.

My experience suggests that in a down market, sellers flock to the national association of realtors who really know their market and produce results, rather than in a frothy market where any realtor will do the trick. Product knowledge is key in a down market.”

Expert Perspective on Housing Bubbles

When there’s limited housing supply and rising supply and demand due to speculation or a deregulated real-estate financing market, we have a housing bubble. It appears that currently, we’re in a housing inventory bubble as home buyers overpay on home sale prices in hot real-estate markets and investors compete with cash on overpriced homes. A housing bubble typically lasts for four to five years.

According to Wikipedia, “Bubbles in housing markets are more critical than stock market bubbles. Historically, equity price busts occur on average every 13 years, last for 2.5 years, and result in about 4 percent loss in GDP. Housing prices busts are less frequent, but last nearly twice as long and lead to output losses that are twice as large (IMF World Economic Outlook, 2003).”

Eventually, home price growth rises to a point where there isn’t a demand to sustain it, and it stagnates or falls — i.e., a sharp drop in home prices or an estate bubble burst.

What Is a Housing Market Bubble?

A housing bubble is the definition of supply and demand personified. The demand for houses increases as homebuyers flood the market seeking their dream house. Speculators and investors also enter the arena and immediately snag investment properties (increasing the cost of rent) and snag fixer-upper properties for a quick flip.

One thing to remember is that a housing bubble is always a temporary event. The stock market experiences bubbles that are similar, but stock investors know the risks – what goes up must come down. Like the tide – comes and goes. However, many homeowners honestly believe that the value of their house will rarely decrease dramatically so when the bubble pops many are in denial at first.

A housing bubble is always a temporary event. The bubble can last for a few years but will eventually flatten which is what is starting to occur in 2022. Mortgage rates are increasing which drives up the cost of the monthly mortgage payments and quickly makes them out of reach for most homebuyers. Investors also start to get nervous and put the skids on seeking houses to flip. As everything snowballs, the bubble starts to collapse.

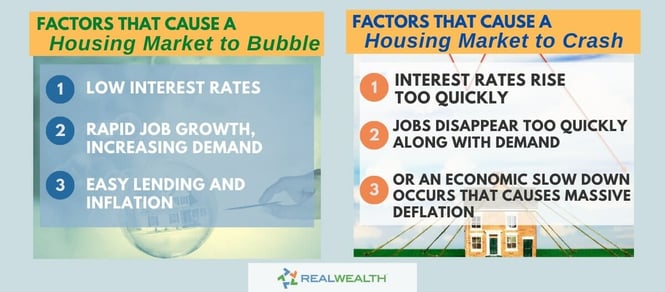

What Causes a Housing Market Bubble?

Most see a housing bubble because of artificially inflated prices. The rapid increase in demand coupled with the speculation of investors, low inventory, low mortgage interest rates, and somewhat loose credit standards. The entire cycle becomes savage with low interest rates fueling buying which causes the supply to plummet. To curtail the rampant inflation, the Fed increases mortgage interest rates, but that causes monthly payments to rise to levels that are too high for a common homebuyer to afford.

A standard homebuyer quickly finds themselves unable to find an affordable home. The increase in mortgage interest rates and a slight increase in inventory only continue to make it more difficult for home buyers who are often just being priced out of the market completely.

What Drives Housing Demand?

Many things drive housing demand:

- Economic activity increases when prosperity builds. Consumers have more disposable income so start to pursue home ownership.

- Low mortgage rates help to create affordability.

- Mortgage deals such as low monthly payments for some help to create accessibility to a demographic that might not otherwise be able to afford to purchase a home.

- Lowered standards for underwriting provide easy access to credit.

- Lenders start to seek mortgage business to meet the growing demands of Wall Street which want mortgage backed securities (MBS) that offer a high yield.

- Mortgages become easier to obtain due to looser lending standards.

- Borrowers become more willing to take risks.

- Home buyers and investors start to indulge in risky behavior which is a part of the unrealistic home price appreciation.

Every bubble has an uptick in the housing market activity

Why Does a Housing Bubble Burst?

A housing bubble will inevitably burst if the prices start to become unrealistic and risk-taking becomes commonplace.

Builders will often continue to build even if the demand has slowed or taken a nosedive. Supply will increase and demand will decrease.

When the sales start to slow but the prices rise, then realities of risk start to create waves in the market. Prior to the impact of the realization, several things occur.

- Interest rates increase which makes it virtually impossible for many buyers to afford to buy a home. In some situations, current homeowners also start to experience hardship if their current home loan does not have a fixed interest rate. Defaults and foreclosures start to happen which can increase the home inventory substantially.

- Economic activity starts to slow, unemployment usually increases, and a reduced number of job openings occurs as the recession firmly takes hold.

- Demand starts to burn out, so supply and demand become almost equal which leads to a slowing of home price appreciation.

- Credit standards become more difficult.

- Investors and speculators jump ship by leaving the market

- Prices plummet.

What to Do in a Housing Bubble

Are you a homeowner in an area where the prices of homes have started to soar? If so, you are probably thinking about selling. However, unless you have plans on moving to a more affordable area, renting, or downsizing then you’ll just be selling and climbing right into the bubble. Once your home sells, you’ll have to purchase another house which means you will be competing to buy a house in an overly inflated market. You don’t want to end up overpaying.

The 2007–08 Housing Bubble and Housing Market Crash

During the mid-2000s, a housing bubble occurred followed by a recession. The entire process was not immediate. In fact, it took years to occur, but the entire process followed the standard pattern with pricing increases, low interest rates, lax lending, and low-down payments. The entire situation encourages people to borrow more debt than they could comfortably afford. The rapid fire homebuying started to drive the prices of real estate up.

Eventually, most speculative investors stopped investing because of the escalated risk. Many completely jumped ship and got out of the mix. Eventually, the economy started to spiral, subprime borrowers were unable to make their mortgage payments and they could not refinance them for less.

Home prices started to grow, and mortgage-backed securities were quickly sold off. Eventually, mortgage defaults started to occur, and foreclosures skyrocketed.

What’s Different From the 2008 Housing Market Crash?

Even though the Feds are pushing mortgage interest rates up to curb inflation, most do not foresee a crash that is comparable to what occurred in 2008. Even if the economy takes a nosedive, the housing market will not undergo a drastic hit.

Following 2008, laws and regulations were instigated to halt predatory lending. In the last two years, lenders have only been issuing loans to qualified borrowers - unlike in 2008.

How Does a Recession Typically Impact the Housing Market?

During a recession, people face a lot of stress which slows down the housing market. People are too worried about finding employment, layoffs, and other hardships to think about making a big decision like buying a house.

What Conditions Could Lead to a Housing Market Crash or Housing Bubble Burst?

If the bubble does start to flatten and burst, signs will start to occur that indicate instability.

- Increased employment. When people start losing their jobs then the housing market becomes inundated with desperate sellers which causes an increase in distressed home sales. Foreclosures also start to become commonplace.

- Homebuilding starts to slow down.

- Buyer demand can start to slow.

- Homebuyer motivation cools.

What Factors Cause a Housing Market to Crash?

A housing market does not just crash. In 2022, the housing market might not crash but that is not to say it won’t crash eventually.

First a housing bubble starts to form which is fueled by low interest rates, job growth and easy lending. Once the bubble has developed, it can easily pop if one of the three factors is removed from the equation.

A housing market crash will occur if the following happens:

- Interest rates increase.

- The job market dries up.

- Lenders make loans harder to get .

- An economic downturn occurs.

If there are too many homes with a high-priced tag on the market and no one to buy the houses, then the prices start to fall - the bubble pops.

What Is Mean Reversion?

Homeowners often believe that the price of their home will hold into the future. However mean reversion eventually occurs and price appreciation.

The market goes through times of rapid appreciation but eventually depreciation also occurs and then the price point aligns with the long-term average rate of appreciation which is known as the reversion to the mean.

Following rapid price appreciation (or depreciation) the prices will revert to where they should be due to long term average rates of appreciation.

With home prices, the mean reversion might occur gradually or quickly. Home prices can rapidly climb to a point that puts them in line with the long-term average or they may simply stay constant, and the long-term average will catch up.

Price Appreciation Estimates

Home buyers use price performance as a benchmark, so the estimate is typically unrealistic and usually only leads to risks. Too much risk taking happens when picking a mortgage and deciding on the size/cost of home that a buyer purchases. Short term mortgages are often pushed to buyers who are willing to take risks. They pick the mortgage and believe that they will refinance in a few years based on the climbing equity in the home, but sometimes it becomes only wishful thinking.

Recent price performance of a home does not predict the price performance in the future. Homebuyers need to consider the long-term rate of home appreciation along with mean revision before making a financial decision.

Are We in a Housing Bubble Now?

There has been a period of rapid market value growth in the last two years. Home prices have climbed and there exists a low supply of houses. Even as mortgage interest rates have risen in recent months, putting pressure on housing affordability, the decrease in homebuyer interest has been relatively measured. Most would agree that a housing bubble exists at this time.

So…Will the housing market crash in 2023?

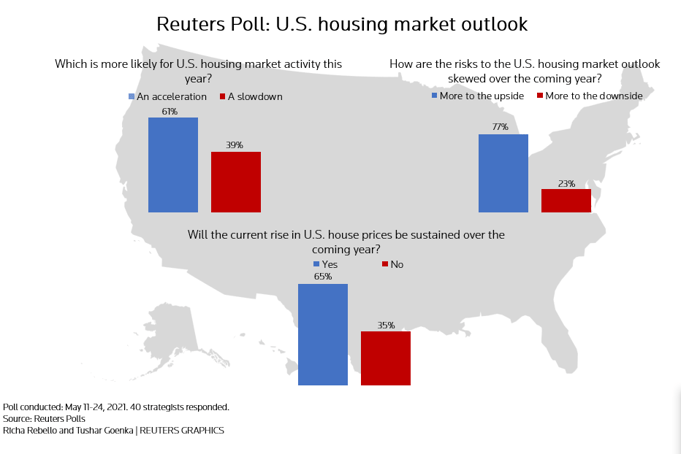

A recent Reuters poll of 40 housing sector analysts suggested that house prices rising in the U.S housing affordability will rise more slowly in 2022. The surveyed analysts estimated that home values would rise by 10.6% this year, followed by a gain of 5.6% in 2022. According to the Reuters report: “Beyond this year, U.S housing prices were forecast to moderate and average 5.6% growth next year and 4.0% in 2023 housing market.”

Experts believe we’ll see the high home values price growth rates reduce to near-normal levels in 2022 and 2023. Another reason why there is probably not going to be a housing market crash in 2022 is that there have been tighter lending standards.

A major reason for the housing market crash of 2008 was that there was a high interest rate of mortgage fraud. The mortgage denial interest rates halved between 1997 and 2003.

The cost of predatory lending practices increased, and the federal reserve loosely supervised banks and lenders, leading to price corrections in many markets. The culmination of these things led to a housing bubble burst.

This led to hundreds of thousands of home prices going into foreclosure, multiple subprime lenders declaring bankruptcy, and the real-estate market requiring federal bailouts.

On the mortgage front, we don’t see the same kind of indiscriminate lending being practiced in the face of new legislation and federal oversight. Yet, there is still uncertainty, since “whatever goes up must come down.” But based on the facts, the housing market crash isn’t about to happen in 2022.

Will the Real Estate Bubble Burst in 2023?

Will the Real Estate Bubble Burst in 2023?No one knows for sure. Many predict the bubble will burst in 2023 but others don’t foresee such a dire prediction.

Many form their guess on whether the bubble will burst based on a report that was released at the end of August 2022 by the S&P CoreLogic Case-Shiller Index which is considered the number one measure for home prices in the nation.

The June 2022 report had revealed ongoing deceleration for price increases. Prices had continued to increase by an 18% annualized rate (the previous month was 19.9%. The Case-Shiller analysis continues to show a slowing in price appreciation, especially in urban areas where prices had risen rapidly over the last two years.

Will prices continue to plummet? At this point, Fitch Ratings shows that the prices of homes continue to be 11% overpriced. Many foresee a price reduction as the bubble bursts in 2023, especially on the West Coast.

What Causes Housing Prices to Fall?

When mortgage rates increase, the demand starts to slow, and the prices come down. An economic slowdown also impacts home prices. As baby boomers start to retire, they often head to Florida or Arizona to retire which causes prices in their home states to cool.

Local factors can also cause housing prices to fall. As the economy starts to slump, job losses occur in many cities that are difficult to find work within. Crime rates often climb. In other regions, tax changes or local services might change making the area less attractive.

Which Housing Markets Are Most Overvalued in 2022?

The Florida Atlantic University and Florida International University carried out a study that outlined the 10 most overvalued cities in the nation. In first place is Boise City, Idaho followed by Austin, Texas.

The other cities that made the list of the most overvalued in 2022 include:

- Atlanta, Georgia

- Ogden, Utah

- Provo, Utah

- Fort Myers, Florida

- Spokane, Washington

- Las Vegas, Nevada

- Salt Lake City, Utah

- Phoenix, Arizona

Should I Buy a Home Now or Wait?

At this time, the big question every would-be homebuyer wants to know is, “Should I buy a home now or wait?” Purchasing real estate is a big decision. In fact, buying a house is the single biggest purchase any person will probably ever make. To ensure home buying success, a buyer needs to make the decision only when they are in a strong financial position.

The choice to buy a house should never be made lightly. Instead, a buyer needs to do their research. A mortgage calculator will help a buyer figure out their monthly housing costs by inputting the projected down payment and interest rate.

No one can predict with 100% accuracy what will happen in the next year. Instead, a buyer needs to make the decision on whether to buy by examining their needs and budget. If you must make sacrifices to buy a house, then it's common to end up struggling and have a bad case of buyer’s remorse. Never overpay for a house or it will become a dead weight around your neck which you might not be able to unload if the market does turn sour.

Tips for Buying in a Hot Housing Market

At this point, the most important thing a home buyer can do is set a budget and do not deviate. Even with more homes coming up for sale, prices remain high and mortgage rates are climbing. Buyers and sellers are not meeting in the middle at this point. Right now, in late 2022, there exists a big disparity between buyer and seller with buyers consistently trying to lowball but sellers holding firm because they still expect last year’s prices.

Despite the tide changing ever so slightly in the housing market, it remains a seller’s market, so buyers must remain cautious and not overspend.

Tips for Selling in a Hot Housing Market

If you plan on selling your home, then you’ll want to find a strong listing agent who has exceptional referrals and who clearly understands and knows the area. A good agent will price your home accordingly while still bringing all offers to the table from buyers.

Sellers need to be realistic. You cannot expect 2021 prices in 2022. Things are changing.

Always present your home in the best light by tackling the following before ever listing:

- Small renovations or repairs

- Decluttering

- Focusing on curb appeal

- Optimizing lighting

- Cleaning up the property.

- Focus on making the space seem spacious

With the uptick in homes for sale, a seller’s competition is increasing so you’ll need an edge to grab buyer’s attention and bring in offers. With greater inventory, home buyers won’t be as desperate as they were last year or the year before last, so you need to bring your A-game to sell for a top price.

Housing Market Predictions In 2022: Will Prices Drop?

As 2023 get closer, home prices show no significant slowdown even with higher mortgage rates and a steadily increasing housing supply. The market remains resilient with strong prices. In June it attained a median home price record high of $413,800 but in July it did take a downward turn plummeting to $403,800, as reported by the National Association of Realtors (NAR).

Whether the drop in price in July is due to the normal seasonal housing slump that always occurs as autumn arrives remains to be seen. Either way, July’s sales price was still a strong 11% higher than 2021. The high housing costs coupled with an increase in mortgage interest rates have impacted housing applications because the Mortgage Bankers Association (MBA) reports that they are at their lowest in 22 years. At this time, the MBA is giving the possibility of a mild recession occurring a 50% chance in the next 12 months, but those projections can change.

The housing market swings like a pendulum due in part to the economy coupled with a good portion of consumer sentiment. The economy shows significant signs of weakening as depicted by the gross domestic product (GDP). The GDP has slumped over the last two quarters which has led economists to project that there is a recession on the horizon even though some aspects contradict the dire projections such as a strong job market and continued consumer spending.

Will Home Prices Continue to Rise?

Record high home prices coupled with rising mortgage rates are making it a nightmare for home buyers to find affordable housing. Zillow has reported that in 2022 a mortgage payment is 76% higher than it was in 2019 but earnings remain virtually unchanged for most homebuyers with only small gains of around 5% which still puts them way behind the current inflation increases.

MBA economists report that home prices will increase by 9.9% as 2022 winds down and then in 2023 there will be a 3.1% increase. With the rising home prices and the increasing interest rates, homebuyer dreams of affordable housing are becoming quickly unattainable.

Housing Inventory Predictions for 2022

Even though real estate prices will continue to rise, the inventory is also going to increase. In July 2022, inventory rose 31% compared to the previous year. Many see the increase in homes for sale as a positive thing because it creates greater balance in the industry. Home buyers will have more options.

Housing Market Predictions for 2022-2026 (Is the Crash Coming?)

It’s easy to get blindsided when it comes to real estate. No one has a crystal ball and all you can do is make an educated guess. Many knew in 2006, 2007, and 2008 that borrowers would be unable to make their payments due to lax lending and adjustable-rate mortgages. Borrowers, bankers, and mortgage brokers started to ‘change’ numbers to ensure a home loan. Mortgage brokers gave out large loans with no money down and asked for no verification of assets or income.

The rampant lending that occurred in 2006,2007, and 2008 was causing the bubble to grow, but a pop was inevitable. Easy lending in hot real estate regions like Las Vegas caused the average home price to double in only a year. It was a house of cards waiting to fall and foreclosures would soon flood the market. Market cycles are a reality and need to be weighed by anyone considering making a home purchase.

During times of flux, investors stop buying in overpriced areas and look at regions where job growth is strong, but prices are undervalued as a potential place to make an investment. Ideally, wages should always grow faster than home prices if you are considering buying real estate for use as a rental or investment. If the housing bubble starts to flatten or burst, then the cities that have experienced overvaluation will crash, but places where wages have increased but home prices have remained low or stable will more than likely hold steady.

In the real estate world, you will frequently hear the three most important considerations are:

- Location

- Location

- Location

In addition to location, market timing is also important. Is a crash coming in 2023 to 2026? Many foresee a change on the horizon.

14 Nationwide Housing Market Predictions for late 2022

Let’s look at the top 14 nationwide housing market predictions for 2022:

1. Unemployment Rates Will Stay Low

Inflation has impacted American families, but the job market remains strong with low unemployment rates. The Bureau of Labor Statistics shows that in August the unemployment rate increased by 3.7 percent but there were very notable job gains in health care, retail, business services and professional jobs.

In 2020, the COVID-19 pandemic hit, causing many businesses to shut their doors as widespread lockdowns occurred. Millions found themselves jobless and unemployment skyrocketed. The Federal Reserve and the government acted quickly to put money into the pockets of Americans. They issued checks to help stimulate the economy and gave businesses loans that required no immediate repayment. Also they extended unemployment benefits. Americans were able to breathe easier and start savings. The economy has restarted and jobs increased and have continued to grow at a steady rate.

Nowadays, there are ample job opportunities and too few people to fill the openings in many cases. Employers have had to increase their wage and salary rates as they desperately seek employees to fill positions.

2. Job Openings will remain over 10 million

In 2022, life in the business world has returned to a semblance of normal despite the continued uncertainty about the COVID-19 pandemic. Around the world, countries have also re–opened borders and people are again cautiously traveling. In most ways, life has returned to normal (pre-pandemic).

The consumers are again buying goods at a record rate and services have escalated and many businesses have been unable to keep up. During the pandemic, many factories started to close their doors and the global supply chain took huge hits. Now, businesses are struggling to meet the demands of consumers and material shortages continue.

At this point, job opportunities continue, and wage growth is not slowing down. Currently, there are 11.2 million job openings nationwide.

3. Inflation will remain higher than the Fed’s 2% target

The war between Russia and Ukraine has caused shortages. The wheat exports from the Ukraine have practically come to a halt. The price of gasoline has skyrocketed globally. Europe is facing a major shortage in oil and natural gas Russia is one of the world’s largest exporters. The U.S. relies on ally about 4% of oil obtained from Russia, but the uncertainty of the war and the global trade of crude has still impacted prices at the pumps for Americans.

In the last year, rent has also experienced an increase nationwide with many markets such as Phoenix and Miami experiencing a 20% increase in rent prices.

In 2020 and 2021, many homeowners struggled to make ends meet and pay their monthly mortgages due to the COVID-19 pandemic and lockdowns. However, the government and lenders allowed delinquent payments to be placed on the tail end of the loan.

In 2021, four million families who own homes were in forbearance but by 2022 that number is at only one million. With the market’s low inventory, most homeowners will list their home instead of going into foreclosure.

The Feds have increased the supply of money over the last two years by 50% to help increase and fuel the economy as Covid-19 is retained in. With the additional money in circulation the prices continue to increase and fuel inflation.

4. The Federal Reserve will try to fight inflation by raising rates at least three times

The Federal Reserve is trying to curtail inflation. The economists believe that if the feds increase the lending rates then the economy will slow and help stop the uncontrolled inflation. They have said they plan to hike interest rates a proposed seven times.

In 2020, the Feds had lowered interest rates in an effort to lift up the economy and they also started to buy mortgage-backed securities and bonds to ensure that the rates stayed low.

If the Feds raise the rates too rapidly in 2022, then the economy could enter a state of shock and a recession will result. The GDP has already started to slow down, and some economists believe the nation is already in the first stages of a recession.

The increased mortgage rates will make it difficult or impossible for many buyers to afford a home. With fewer home buyers, the competition will decrease. The demand for rental properties will increase if people cannot afford to buy a home which will increase rent and may end up increasing inflation.

5. Mortgage rates will be over 6%

During the Sept 20 to 21, 2022 meeting, the Federal Reserve announced it will raise interest rates by 0.75 percentage point. The Feds have made the decision based on the increasing inflation rates which are the highest they have been in 40 years (8.3% in August). At this point, the Federal Reserve intends to continue raising interest rates until they believe that inflation has been curbed.

Mortgage rates have now hit their highest since 2008 and will continue to increase. The 30-year fixed interest rate is now at 7%.

6. Home prices will continue to climb

As the interest rates climb, the housing market will cool, which isn’t completely disastrous because 2021 was very unhealthy with increased demand and short supply which drove prices sky high. The Idaho capital of Boise saw a price increase in real estate of over 40%. Many theorized that the increase was due to Californians flocking into the area due to the increase in remote work and to escape the soaring prices of Los Angeles and other areas. However, the migration has caused prices to skyrocket and has quickly out-priced locals from being able to own a home.

An increase in prices for homes was also fueled by 2021’s reduction in interest rates. After the lockdowns of 2020, many millennials decided they needed freedom with an increase in square footage after being cooped up in small apartments, so they quickly started looking for homes versus apartments and condos.

Since 2020, working from home has become commonplace with many businesses embracing the practice as they focus on doing away with costly office space. Nowadays the sky's the limit for people who have lucrative salaries. Working from home lets them live anywhere. They can move out of cities and into the country or suburbs.

Florida and many other places have experienced a huge surge of people seeking to relocate due to the ability to work remotely. The phenomenon has caused home prices to climb in many areas where prices were once low or stable.

7. There will be an uptick in mortgage defaults

In the last couple of years, foreclosure rates have been low. The Biden administration has been providing assistance which lasted until July 21, 2021 and let people miss their mortgage payments. However, in 2022, the foreclosure rate has increased by 150%. Metro areas have been hit hard with 96% seeing an increase. The hardest hit states are Ohio, Illinois, and New Jersey. Foreclosure starts are also growing in California, Tennessee, and Florida.

An increase in delinquency is occurring in FHA and VA loans. In many cases, FHA lenders were more lenient on credit scores and would take a reduced down payment. The lenience has put them in a precarious position as many FHA borrowers have started to default on the loans.

Conventional loans were only given to borrowers with high FICO scores. The borrowers for such loans had strong wage growth and purchased homes with impressive equity so are not experiencing a high rate of foreclosures in 2022.

Foreclosures are managed differently in different stats. In some it can take a few months and in others it will take a few years for a bank to repossess property.

Stagnant markets will be the hardest hit because those facing foreclosure will have a challenging time selling their properties.

8. More people will choose adjustable-rate mortgages

The Millennial generation continues to fuel the first-time homebuyer pool. They are independent and well-educated. Most are willing to lock in a fixed rate mortgage for a decade and then face adjustment instead of continuing to pay high rents. An ARM interest rate for seven years is lower than a fixed interest rate. The lower interest can often make all the difference about whether the home buyer can afford the property or not.

In some situations, a homebuyer might not plan to live at the residence for longer than a decade, so the adjustable-rate mortgage makes the home more affordable than a fixed rate mortgage for 30 years. Borrowers need to know that an 5- ARM the rate will remain fixed for the set time period and then adjust every year after.

Short term loans have a substantial amount of risk because there is no way to forecast the market. Interest rates might be substantially higher, and a home’s value might plummet instead of climbing. It might be hard to sell fast or it could be easier. There’s simply no way to know for sure which makes things risky.

Currently, many borrowers believe that the prices will remain high in the future, and they will have had the opportunity to pay down part of the balance which increases their equity before the interest rate might climb.

9. Lending requirements will tighten

Easy lending standards will start to stall in 2022. Obtaining a loan will become more difficult as the Federal Reserve raises rates to cool off the economy.

The Federal Reserve will assess any decline in the prices that might impact commercial properties and look at any issues with corporate bond markets.

The MBA reports that a reduced Mortgage Credit Availability Index (MCAI) means that getting a loan is going to be harder and mortgage credit will continue decreasing in 2022. With money being removed from the market, banks have less money that they are willing to loan out. Banks are going to become even more picky and only lend to uniquely capable borrowers, especially with the Feds attempting to put the brakes on the wildfire inflation. .

Increased interest rates and stiffer lending is going to make it harder for borrowers to qualify. Many won’t be able to buy a home so will end up renting. With so many people renting, the price of rent is going to increase which usually spikes inflation which is going to become a problem with the Feds trying to reduce inflation.

10. More people will choose to work remotely to lower their costsDuring 2020, many organizations had to relearn how to function with their workforce staying home due to mandatory lockdowns. Technological innovations like Zoom and other platforms let workers continue to function remotely.

Companies can now hire skilled talent from anywhere in the world due to embracing a remote workforce. They have also been able to eliminate costly office space. Remote workers can move out of metropolitan areas where the price of housing has been historically expensive to more affordable suburban or rural locations.

11. The suburbs and exurbs will become more expensive

The housing market in family friendly areas continues to grow as Millennials continue buying homes. Many are seeking homes in the suburbs because of the school districts and the family friendly environment. However, they are pushing the price of homes higher in such locations. Competition in such locations is also intensifying which makes affordable housing hard to find.

Studies show that the most popular areas for millennial home buyers include:

- Denver, Colorado

- Seattle, Washington

- Boston, Massachusetts

- Miami, Florida

- Jacksonville, Florida

- Tampa, Florida

12. The number of renters and rental prices will rise

The price of rent is souring nationwide with many areas such as Miami, Austin, and Phoenix experiencing a 40% increase. As the supply shortage continues, the cost of rent increases. The increasing mortgage rates will also impact rent and cause prices to continue escalating.

Inflation has made any increased salaries or wages obsolete, so anyone faced with paying rent is probably struggling to pay their monthly expenses. The price of building affordable housing has always increased so with rent increasing and less affordable housing available, people seeking to rent are going to have a tough time finding an available rental.

13. Biden’s Proposed Tax Increases happen due to November elections

The U.S. president has proposed a tax hike on those who are valued at over $100 million. This tax increase would impact few households with most of the tax paid by billionaires. The wealthiest have benefited from the nation’s rapid growth and the government wants to collect tax. Despite the proposal, many doubt that any tax increases will happen.

14. Investors will flock to real estate and stocks

Investors are going to start taking notice of both stocks and real estate in 2022 due to inflationary assets. Historically, investors will purchase bonds and mortgage-backed security because they are safe but at this point an investor will lose money on bonds. Most are forecasting inflation so they are purchasing assets which they believe will grow. Many are focusing on real estate as an investment.

11 More Housing Market Predictions For 2022, 2023, 2024, 2025 AND 2026

No one has a crystal ball, but below are a few top real estate predictions:

-

Interest rates continue to climb throughout the next couple of years.

-

Real estate prices will increase in areas that millennials want to live in.

-

Home buyers will avoid selling because they have a locked-in low interest rate.

-

The number of houses for sale will become even more tight.

-

Fewer homes will sell or enter pending.

-

buyers will snap up any houses for rent.

-

Agents who are willing to list will become a hot commodity, but buyers’ agents face the possibility of having to lower their fees.

-

By 2025, there will be a smaller pool of agents.

-

The few agents who manage to hold on will end up offering more services.

-

More data will become available.

-

People might weigh the benefits of home sharing opportunities.

Finally, The Big Yearly Question: Will the Housing Market Crash In 2022?

With 2022 almost over, the market is probably not going to crash this year. Many fear a crash like 2008, but many factors make such a crash unlikely. There are tighter lending standards which minimize the risk. The loans that lenders have made are strong and buyers have savings, low debt, and high credit scores so a crash is not likely to occur at this point.

Will The Housing Market Crash in The Next 5 Years?

In the next five years, major changes are on the horizon in the housing market. The economy will fluctuate but experts do not forecast a major housing market crash. However, many housing markets in the nation are going to take an impact, especially major metropolitan areas.

The expensive real estate and prohibitive cost of living in the cities means that many will move away from the areas to suburbs or other smaller towns. Real estate investors are scrambling to figure out where people will move so they can determine which markets to invest in.

When Will the Housing Market Crash?

When the economy is in a state of upheaval, people struggle to make a financial decision such as buying a house. Most do not foresee the housing market crashing in the near future, but many things will play a part in what happens such as:

- Housing demand

- Housing supply

- Interest rates

- Unemployment

At this time, one thing most can agree on is that there is going to be a period of slow growth.

Final Thoughts

What will you do if there is a real estate market crash in 2022?

The key to navigating a housing market crash is having a good strategy in place. During the 2008 housing market crash, realtors and real estate investors who embraced innovative marketing strategies grew their businesses even while the overall current market declined. While a housing market crash isn’t expected in 2022, it’s still a good idea to plan for every eventuality.