In apartment syndications, the general partner (GP) catch-up is a distribution to the GP such that they have received their full portion of the profits.

The GP catch-up is relevant when the compensation structure of the partnership between the GP and the limited partner (LP) includes a profit split.

For example, let’s say the LPs are offered a 7% preferred return and the profit split is 70% to the LPs and 30% to the GPs. At the conclusion of the partnership, 70% of the total project cash flow (ongoing cash flow and profits from sale) must have gone to the LPs, and the remaining 30% must have gone to the GPs.

There are two main types of GP catch-ups. The most common is a GP catch-up at sale. The other, less common, is an ongoing GP catch-up.

The advantage of the ongoing GP catch-up is that the GPs can receive distributions immediately rather than waiting until sale.

Whichever GP catch-up you decide to pursue, make sure it is properly defined in your waterfall in the PPM.

To explain how each of these two GP catch-ups work, let’s use the following dataset as an example:

- Preferred Return to LPs: 7%

- Profit Split (LP/GP): 70/30

- LP Equity Investment: $1,000,000

- Year 1 to 5 Cash Flow

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 |

| ($1,000,000) | $71,000 | $77,000 | $84,000 | $93,000 | $130,000 |

- Profit at Sale (After $1,000,000 in equity is returned): $1,500,000

GP Catch-Up at Sale

For a GP catch-up at sale, the LPs receive their preferred return first. Then, the profits above the preferred return are split 70/30. At sale, after the LP equity is returned and before the profits are split 70/30, a catch-up distribution goes to the GP until they have received 30% of the cumulative cash flow up to this point.

Here is a breakdown of the ongoing distributions to LPs and GPs:

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| Total | $(1,000,000) | $ 71,000 | $ 77,000 | $ 84,000 | $ 93,000 | $ 130,000 | $ 455,000 |

| LP | $ 70,700 | $ 74,900 | $ 79,800 | $ 86,100 | $ 112,000 | $ 423,500 | |

| GP | $ 300 | $ 2,100 | $ 4,200 | $ 6,900 | $ 18,000 | $ 31,500 |

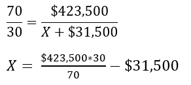

Based on the “Total” column, the LPs have received 93.08% of the profits and the GPs have received 6.92% of the profits. Therefore, the first portion of the $1,500,000 profit at sale goes to the GP until they have received 30% of the total profits.

Here is how you calculate that amount:

X equals $150,000.

After the $150,000 distribution, the LP has received $423,500 and the GP has received $181,500, and the 70/30 split is achieved.

The remaining profits, $1,350,000, are split 70/30. This equates to $945,000 to the LP and $405,000 to the GP.

Here is the updated data table for cash flows to the LP and GP:

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| Total | $(1,000,000) | $ 71,000 | $ 77,000 | $ 84,000 | $ 93,000 | $ 1,630,000 | $ 1,955,000 |

| LP | $ 70,700 | $ 74,900 | $ 79,800 | $ 86,100 | $ 1,057,000 | $ 1,368,500 | |

| GP | $ 300 | $ 2,100 | $ 4,200 | $ 6,900 | $ 573,000 | $ 586,500 |

The total distribution is $1,955,000. $1,368,500, or 70%, went to the LP. $586,500, or 30%, went to the GP.

Ongoing GP Catch-Up

With an ongoing GP catch-up, the LPs still receive their preferred return first. However, before the remaining profits are split 70/30, the GP receives a promoted catch-up distribution. This distribution is equivalent to a 70/30 split.

Here is how that amount is calculated:

X equals 3.

Therefore, the GP receives a 3% return based on the total LP equity investment. Any unpaid GP catch-up is accrued and paid out when possible. Once both the LP and GP have been paid, the remaining profits are split 70/30.

Since our sample equity investment is $1,000,000, the LP receives $70,000 annually and the GP receives $30,000 annually.

Year 1 Cash Flow is $71,000, which means the LP receives $70,000, the GP receives $1,000, and $29,000 is owed to the GP.

Year 2 Cash Flow is $77,000, which means the LP receives $70,000, the GP receives $7,000, and an additional $23,000 is owed to the GP. The total amount owed to the GP is $52,000.

Year 3 Cash Flow is $84,000, which means the LP receives $70,000, the GP receives $14,000, and an additional $16,000 is owed to the GP. The total amount owed to the GP is $68,000.

Year 4 Cash Flow is $93,000, which means the LP receives $70,000, the GP receives $23,000, and an additional $7,000 is owed to the GP. The total amount owed to the GP is $75,000.

Year 5 Cash Flow is $130,000, which means the LP receives $70,000 and the GP receives $30,000. The remaining $30,000 also goes to the GP to pay down the accrued amount. The total amount owed to the GP is now $45,000.

At sale, after the LP equity is returned, the accrued amount owed to the GP, $45,000, is distributed. Then the remaining profit, $1,455,000, is split 70/30. The LP receives $1,018,500 and the GP receives $436,500.

Here is the data table for cash flow to the LP and GP:

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Total | |

| Total | $(1,000,000) | $ 71,000 | $ 77,000 | $ 84,000 | $ 93,000 | $ 1,630,000 | $ 1,955,000 |

| LP | $ 70,000 | $ 70,000 | $ 70,000 | $ 70,000 | $ 1,088,500 | $ 1,368,500 | |

| GP | $ 1,000 | $ 7,000 | $ 14,000 | $ 23,000 | $ 541,500 | $ 586,500 |

As you can see, the “Total” five-year distributions to the LPs and the GPs are the same for each catch-up type. However, for the ongoing GP catch-up, the GPs receive more money sooner, which — in turn — means that the LPs receive money later. As a result, the LP internal rate of return (IRR) is lower with the GP catch-up.

| Year 0 | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | IRR | |

| At Sale | $(1,000,000) | $ 70,700 | $ 74,900 | $ 79,800 | $ 86,100 | $ 1,057,000 | 7.390% |

| Ongoing | $(1,000,000) | $ 70,000 | $ 70,000 | $ 70,000 | $ 70,000 | $ 1,088,500 | 7.320% |

Therefore, the GP catch-up at sale is more advantageous for the LPs and the ongoing GP catch-up is more advantageous for the GPs, even though both the LP and the GP receive the same total cash distributions in each scenario.

About the Author:

Joe Fairless is the co-founder of Ashcroft Capital, a fully integrated multifamily investment firm with more than $2.7 billion in assets under management, and the founder of Best Ever CRE. His podcast, the Best Real Estate Investing Advice Ever Show, is the world's longest-running daily real estate podcast with more than 500,000 monthly downloads.

Disclaimer:

The views and opinions expressed in this blog post are provided for informational purposes only and should not be construed as an offer to buy or sell any securities or to make or consider any investment or course of action.